MBA

MBA ProgramsBest MBA Programs for Investment Banking in 2026

Which business schools actually get you into Goldman Sachs, JPMorgan, and Evercore — ranked by real recruiting outcomes.

Every article is researched and written with academic rigor and industry experience to sharpen your decision-making.

Real-time performance of key indices, commodities, and asset classes relevant to finance professionals.

📥 Free: Wall Street Recruiting Checklist

20 steps to break into investment banking — download instantly

Our aggregator pulls headlines from leading financial media with full copyright respect: we only show public RSS feed excerpts with a direct link to the original source.

See Financial NewsIn-depth analysis of curricula, costs, alumni networks, and return on investment for each program.

Which business schools actually get you into Goldman Sachs, JPMorgan, and Evercore — ranked by real recruiting outcomes.

An honest head-to-head comparison of the two most prestigious finance MBA programs — curriculum, network, and placement.

A frank ROI analysis: tuition costs, salary uplifts, payback periods, and when the MBA makes no financial sense.

Cost, time, career outcomes, and which one actually opens the doors you need — a practical framework for your decision.

Essays, recommendations, leadership stories, and the application mistakes that eliminate strong candidates every cycle.

The complete guide for serious candidates: which programs open doors to Goldman Sachs, PE firms, and top hedge funds.

First-year core courses, the case method, AI integration, second-year electives, and whether HBS is worth the investment.

Core curriculum, finance specialization, Wall Street recruiting dominance, and whether Wharton is worth it in 2026.

Whether an MBA is worth $200k+ in 2026 when AI is automating finance tasks — honest analysis with ROI data for top programs.

A direct comparison of MBA vs Master in Finance in 2026 — cost, duration, recruiting access, ROI, and which degree fits your goals.

An honest breakdown of MBA admissions consulting in 2026 — who benefits, real costs, and whether you need it for Harvard or Wharton.

A complete guide to deferred MBA programs in 2026 — Harvard 2+2, Stanford GSB, Yale Silver Scholars, Wharton M2A, MIT Sloan, and Columbia.

Career paths, updated salaries, and strategies to maximize your professional trajectory in finance.

The timeline, the networking playbook, the superday format, and what banks actually evaluate beyond your GPA.

How PE firms actually recruit, what the work looks like day-to-day, and the compensation structure most candidates misunderstand.

Strategies, hiring paths, what analysts do all day, and why compensation is both higher and more volatile than banking.

Day-to-day differences, salary comparison, work-life balance, and which exit opportunities each career actually creates.

Where to intern, how to get selected, and why your summer analyst program is the most important recruiting step of your career.

What VC firms do, how they recruit, what they pay, and the path into the industry for MBA graduates and operators.

Banking, PE, VC, consulting, corporate finance — what each career actually involves and which fits your personality.

What M&A bankers do, how deals work, the skills that matter most, and where bankers go after 3 years in the industry.

An honest analysis of consulting layoffs, what McKinsey, BCG and Bain are actually hiring, and whether consulting is still worth pursuing after your MBA.

Educational technical content on valuation, financial modeling, and portfolio management to establish content authority.

The three-statement model, DCF, LBO, and comparable companies — what you must master before your first finance interview.

Real compensation data for IB analysts, PE associates, hedge fund PMs, and consultants — base, bonus, and total comp.

The formatting rules, bullet-point structure, and technical skills section that get resumes past finance recruiter screens.

Research analyst to PM — how long it takes, what firms value, compensation at each level, and the skills that advance careers.

What M&A bankers do, how deals work, the skills that matter most, and where bankers go after 3 years in the industry.

Strategies, hiring paths, what analysts do all day, and why compensation is both higher and more volatile than banking.

From GMAT to statement of purpose: everything you need to build a competitive MBA application.

Essays, recommendations, leadership stories, and the application mistakes that eliminate strong candidates every cycle.

The formatting rules, bullet-point structure, and technical skills section that get resumes past finance recruiter screens.

A frank ROI analysis: tuition costs, salary uplifts, payback periods, and when the MBA makes no financial sense.

Where to intern, how to get selected, and why your summer analyst program is the most important recruiting step of your career.

An honest head-to-head comparison of the two most prestigious finance MBA programs — curriculum, network, and placement.

Which business schools actually get you into Goldman Sachs, JPMorgan, and Evercore — ranked by real recruiting outcomes.

Week-by-week plan, score targets by school, Quant and Verbal strategy, and the best resources for working professionals.

Curated headlines from the world's leading financial sources

Click "Refresh Feeds" to load the latest financial headlines

Real-time charts and market data — equities, fixed income, forex, and commodities. Powered by TradingView.

An editorial project created by finance professionals with real experience in investment banking and executive education.

MBA Finance Guide was born from a real need: finance professionals aspiring to an MBA face a serious information barrier. The most comprehensive resources are often scattered, generic, or fail to bridge academic theory with the realities of the job market — especially for candidates targeting Wall Street and global financial hubs.

Our team has spent over a decade in the trenches of investment banking, private equity, and high-level financial consulting. We have gone through the MBA admissions process ourselves, worked at funds in New York and London, and now dedicate part of our time to passing on that knowledge with rigor and honesty.

We typically respond within 48 business hours. For personalized consulting inquiries, please mention it in your message.

Your information will never be shared with third parties.

We offer 1:1 consulting sessions of 60 minutes to review your profile, define your program shortlist, and design your application strategy.

Request a Session →MBA Finance Guide operates the website accessible at mbafinanceguide.com. For privacy-related inquiries, please contact us at: mbafinanceguide@outlook.com.

Data processing is based on: (a) the user's consent when completing the contact form; (b) legitimate interest for anonymous statistical traffic analysis. For California residents, we comply with the California Consumer Privacy Act (CCPA).

You have the right to access, correct, delete, object to processing, and request portability or restriction of your personal data. To exercise these rights, please email mbafinanceguide@outlook.com.

This site uses Google AdSense to display advertising. Google may use cookies to show ads based on your prior visits to this or other websites. Users can opt out of personalized advertising by visiting Google Ad Settings.

Contact form data is retained for a maximum of 2 years from the last contact. Anonymized analytics data is retained for 26 months.

This website, accessible at mbafinanceguide.com, is owned and operated by the editorial team of MBA Finance Guide. Contact email: mbafinanceguide@outlook.com.

MBA Finance Guide is an editorial information and education portal covering Finance MBA programs, finance careers, and related topics. All content is strictly informational and educational in nature and does not constitute personalized financial, investment, legal, or academic advice.

All original texts, graphics, logos, images, and other content published on this site are the property of MBA Finance Guide or its authors and contributors, protected under applicable intellectual property law. Reproduction, distribution, or public communication without express written authorization is strictly prohibited.

MBA Finance Guide does not guarantee the accuracy, completeness, or timeliness of the information published. Salary data, rankings, and statistics are estimates based on public sources and may not reflect current market conditions. Users assume responsibility for how they use the information provided.

This site is monetized through Google AdSense. Advertisers are selected automatically by Google, and MBA Finance Guide does not endorse or take responsibility for any products or services advertised.

This legal notice is governed by the laws of the United States. Any disputes arising from the use of this website shall be resolved in the competent courts of the applicable jurisdiction.

Investment banking remains one of the most competitive industries in the world, and in 2026, elite MBA programs still play a massive role in recruiting.

While many students believe technical skills alone are enough, the reality is more complicated. Top investment banks continue to recruit heavily from a small group of business schools with strong alumni networks and direct recruiting pipelines.

For ambitious professionals targeting firms like Goldman Sachs, Morgan Stanley, JPMorgan, or Evercore, choosing the right MBA can significantly impact salary potential, networking access, and long-term career growth.

Wharton remains one of the strongest MBA brands for finance careers.

The school has deep relationships with:

Many students pursuing M&A, valuation, or private equity recruiting prioritize Wharton because of its finance-heavy culture and powerful alumni network.

Harvard Business School continues to dominate because of its global prestige and leadership reputation.

While Wharton may be viewed as more finance-focused, Harvard consistently places graduates into:

The HBS network remains one of the most influential professional communities in the world.

Stanford has become especially attractive for students interested in:

Its close connection to Silicon Valley gives students access to some of the most powerful companies and investors in modern finance.

One reason MBA programs remain attractive is compensation.

MBA associates at top investment banks often earn:

However, students should also understand the demanding nature of the industry.

Long hours, high pressure, and intense competition remain common in investment banking.

For many professionals, the answer is yes.

A top MBA can dramatically improve:

But not all MBA programs provide the same ROI.

Students should carefully evaluate:

Among finance students, few MBA debates are more popular than Harvard versus Wharton.

Both schools are considered elite.

Both place graduates into Wall Street.

Both attract ambitious professionals from around the world.

But despite their similarities, the two programs offer very different experiences.

Wharton has long been viewed as the strongest MBA program for finance.

Its curriculum and recruiting ecosystem are heavily connected to:

Students interested in valuation, financial modeling, and M&A often feel naturally drawn toward Wharton.

The school’s analytical culture also appeals to candidates who enjoy technical finance.

Harvard Business School approaches business education differently.

The famous case-method system focuses heavily on:

That broader approach helps Harvard graduates move into:

The global recognition of the Harvard brand also creates opportunities outside traditional finance.

Wharton generally has a stronger concentration of students pursuing investment banking careers.

Major Wall Street firms actively recruit there for:

Harvard also places graduates into top banks, but many students diversify into multiple industries after graduation.

Students who want a deeply finance-focused MBA experience often prefer Wharton.

Students looking for broader leadership positioning and global prestige may prefer Harvard.

Ultimately, both schools remain among the most powerful MBA brands in the world.

Investment banking recruiting feels confusing from the outside.

Some students receive interviews at elite banks surprisingly early.

Others apply online repeatedly without success.

The reason is simple:

recruiting in investment banking is heavily relationship-driven.

Understanding how the process actually works can dramatically improve a student’s chances of landing interviews.

Top investment banks offer:

That naturally attracts enormous competition.

Banks receive applications from:

Standing out requires much more than strong grades.

Networking remains one of the most important parts of investment banking recruiting.

Students who build relationships with:

often gain major advantages during recruiting cycles.

Many successful candidates spend months preparing before applications even open.

Investment banking interviews frequently test:

Students who ignore technical preparation often struggle during superday interviews.

The most successful candidates usually combine:

Summer analyst internships often function as extended interviews.

Many banks hire full-time analysts directly from their intern classes.

That makes internships one of the most important stages of investment banking recruiting.

Breaking into investment banking is difficult.

But students who understand:

immediately place themselves in a stronger position.

The MBA remains one of the most debated graduate degrees in the world.

Some professionals see it as a life-changing investment.

Others believe business school has become too expensive.

The truth depends heavily on:

Not all MBA programs deliver the same career outcomes.

Top-tier business schools often provide:

Lower-ranked programs may not generate the same opportunities.

That’s why MBA ROI can vary dramatically between schools.

Graduates entering industries like:

can see major increases in compensation.

Many MBA graduates receive:

However, career outcomes still depend heavily on individual execution.

Beyond salary, top MBA programs provide:

Many graduates later describe the alumni network as one of the most valuable parts of the MBA experience.

An MBA can absolutely transform a career.

But students should approach business school strategically rather than emotionally.

The strongest outcomes usually come from:

Technical finance skills matter more than ever in modern recruiting.

Students pursuing careers in:

are increasingly expected to understand financial modeling before graduation.

That’s why students who develop strong modeling skills early often gain a major advantage during recruiting.

Financial modeling involves building spreadsheets that represent a company’s financial performance.

Professionals use these models to:

Excel remains one of the most important tools in the finance industry.

This model connects:

It forms the foundation for advanced financial analysis.

DCF analysis estimates a company’s intrinsic value based on future cash flows.

This remains one of the most common valuation methods in investment banking.

This method compares companies using valuation multiples such as:

Comparable analysis is widely used across finance careers.

LBO models analyze acquisitions funded heavily with debt.

Students interested in private equity eventually need to understand these concepts.

Finance professionals spend huge amounts of time working inside spreadsheets.

Students who improve:

often become much more competitive during interviews.

Financial modeling remains one of the most valuable technical skills in finance.

Students who combine:

position themselves much more effectively for competitive finance careers in 2026.

Few finance careers attract as much attention as private equity.

For many students, the industry represents:

Private equity firms acquire companies, improve operations, and eventually sell those businesses for profit.

But despite the excitement surrounding the industry, many students still misunderstand how private equity recruiting actually works.

Breaking into private equity is extremely competitive.

And unlike investment banking, there is rarely a simple application process.

Private equity firms raise capital from institutional investors and wealthy clients.

They then use that capital to:

Some firms focus on:

The industry can become highly analytical and financially demanding.

Most private equity professionals begin their careers in investment banking.

That’s because banking analysts develop critical skills in:

Many elite private equity firms recruit directly from top investment banking analyst programs.

This is one reason investment banking is often viewed as a gateway into private equity.

Private equity firms typically value:

Candidates are often expected to understand:

Communication skills also matter significantly because professionals regularly interact with executives and investors.

Private equity compensation can become extremely high.

Professionals often receive:

However, compensation varies significantly depending on:

The industry also remains highly demanding and competitive.

Private equity continues to attract ambitious finance professionals because of its:

But students should understand that entering the industry usually requires years of preparation, technical development, and strong networking.

Hedge funds have always carried a certain level of mystery.

Students often hear stories about:

But very few people truly understand what hedge funds actually do.

And even fewer understand how difficult the industry can be to enter.

In reality, hedge funds operate very differently from investment banks or private equity firms.

Success depends heavily on:

Hedge funds manage capital for institutional investors and wealthy individuals.

Their goal is simple:

produce strong investment returns.

Funds may invest in:

Some hedge funds focus on long-term investing.

Others specialize in short-term trading.

Hedge funds often hire smaller teams than investment banks.

That means recruiting can become extremely selective.

Many professionals entering hedge funds come from:

Strong analytical skills are essential.

Hedge funds care heavily about:

Candidates are often expected to:

The ability to think differently from the market can become incredibly valuable.

Compensation in hedge funds can become extremely high.

Top-performing portfolio managers sometimes earn millions annually.

However, compensation is often heavily tied to performance.

That means income volatility can become much higher than in traditional corporate careers.

Hedge funds remain one of the most intellectually demanding areas of finance.

Students interested in the industry should focus on:

The industry rewards performance above almost everything else.

Among ambitious business students, one debate appears constantly:

consulting versus investment banking.

Both careers offer:

But the day-to-day experience inside each industry is very different.

Understanding those differences is critical before committing years of preparation to either path.

Investment bankers primarily work on:

The job is highly financial and analytical.

Bankers spend enormous amounts of time:

The workload can become extremely intense.

Consultants help companies solve strategic and operational problems.

Projects may involve:

Consulting generally involves:

The work tends to be broader and less financially technical than investment banking.

Both industries offer strong compensation.

Investment banking often pays slightly more at the entry level because of:

Consulting compensation remains highly competitive, especially at firms like:

Neither industry is known for perfect work-life balance.

However, investment banking generally involves:

Consulting may involve more travel but often provides slightly more predictable working conditions.

Both careers create strong exit opportunities.

Investment bankers often move into:

Consultants frequently transition into:

Neither consulting nor investment banking is universally better.

The right choice depends heavily on:

Students who enjoy financial analysis may prefer banking.

Students who enjoy broader business strategy may prefer consulting.

Finance professionals often compare two major career credentials:

Both can significantly improve career opportunities.

But they serve very different purposes.

Understanding the difference between these paths is critical for students and professionals planning long-term finance careers.

The Chartered Financial Analyst (CFA) program focuses heavily on:

The curriculum is highly technical.

Many professionals pursue the CFA while working full-time.

The exams are also known for being extremely difficult.

MBA programs provide broader business education.

Students typically study:

Top MBA programs also provide:

For investment banking recruiting, top MBA programs generally provide stronger recruiting access.

Banks recruit heavily from elite MBA programs.

The CFA is respected in banking but is usually more associated with:

The CFA often carries stronger relevance in:

Many hedge funds and asset managers highly respect the designation.

Both credentials can improve compensation.

However, salary growth depends heavily on:

No credential automatically guarantees high income.

The CFA and MBA are not direct substitutes.

They solve different career problems.

Students focused on:

may prefer the CFA.

Professionals seeking:

may benefit more from an MBA.

Finance internships have become one of the most important factors in recruiting.

For students pursuing careers in:

internships can dramatically improve long-term career opportunities.

In many cases, internships function as direct pipelines into full-time jobs.

Employers increasingly expect students to graduate with relevant experience.

Internships help students:

Strong internships also help students perform better during interviews.

Investment banking internships remain some of the most competitive opportunities available to students.

Interns often work on:

Many banks hire full-time analysts directly from their summer intern classes.

Private equity and venture capital internships expose students to:

These internships are often smaller and more difficult to secure than banking roles.

Corporate finance internships can also provide valuable experience.

Students may work on:

These roles help students develop strong financial fundamentals.

Students should focus on:

LinkedIn outreach and alumni conversations can become extremely valuable during recruiting.

Strong internships can completely change a student’s career trajectory.

Students who combine:

often place themselves in a much stronger position for competitive finance careers.

Venture capital has become one of the most attractive careers in modern finance.

The industry sits at the center of:

Many students are drawn to venture capital because of the excitement surrounding startup investing.

But the reality of the industry is often very different from what people imagine online.

Venture capital is highly relationship-driven, extremely competitive, and deeply connected to networking.

Understanding how the industry actually works is essential for anyone hoping to enter the field.

Venture capital firms invest in early-stage and high-growth companies.

Their goal is to identify startups with strong long-term growth potential before those businesses become massive.

VC firms typically provide:

In exchange, they receive ownership stakes in those companies.

If the startup grows successfully, the investment can generate enormous returns.

One major reason venture capital is difficult to enter is the limited number of roles available.

Compared to investment banks or consulting firms, VC firms often operate with very small teams.

Recruiting is also less structured.

Many opportunities come through:

Venture capital firms typically look for candidates who understand:

Strong communication skills matter enormously because venture capital professionals spend significant time:

Analytical ability also remains important, especially when evaluating business models and growth potential.

Compensation in venture capital varies significantly.

Junior professionals may earn less than investment bankers initially.

However, long-term upside can become substantial if investments perform well.

Senior venture capital professionals may benefit from:

Venture capital remains one of the most exciting areas of finance in 2026.

But students should understand that entering the industry requires:

The people who succeed in venture capital often combine analytical thinking with genuine curiosity about innovation.

Few industries generate as much salary curiosity as Wall Street.

Students constantly search for information about:

And while finance compensation can become extremely high, the reality is more complex than many people expect.

Compensation depends heavily on:

Investment banking remains one of the highest-paying entry-level career paths.

Analysts at major banks often receive:

As professionals move into associate and vice president roles, compensation can rise significantly.

However, investment banking also involves:

Private equity professionals frequently earn higher long-term compensation than investment bankers.

In addition to salaries and bonuses, many professionals eventually receive:

At senior levels, compensation can become extremely large.

Hedge fund compensation is heavily performance-driven.

Top-performing portfolio managers can earn enormous amounts during strong market years.

However, compensation volatility also tends to be much higher compared to traditional corporate careers.

Top consulting firms like:

continue offering highly competitive salaries.

MBA graduates entering consulting frequently receive:

Finance compensation often reflects:

The industry rewards professionals who can consistently create financial value.

Finance careers can provide extraordinary earning potential.

But students should evaluate careers based on more than salary alone.

Long-term success also depends on:

In competitive industries like:

small resume mistakes can immediately hurt recruiting chances.

That’s because recruiters often review resumes incredibly quickly.

Students usually have only a few seconds to create a strong first impression.

A well-structured finance resume can dramatically improve interview opportunities.

Finance recruiting follows very specific formatting expectations.

Recruiters generally prefer resumes that are:

Messy formatting can signal poor attention to detail.

That becomes especially problematic in finance careers where precision matters.

Students should clearly list:

Strong GPAs remain valuable in competitive recruiting.

This section carries enormous weight.

Students should focus on:

Strong action verbs improve readability and professionalism.

Finance recruiters often look for skills related to:

Students with technical finance experience often stand out more quickly.

Students frequently damage their resumes by:

Recruiters prefer resumes that communicate impact clearly and efficiently.

Even strong resumes rarely succeed without networking.

Building relationships with:

can dramatically improve recruiting outcomes.

A strong finance resume combines:

Students who invest time improving resume quality often improve their interview opportunities significantly.

Finance offers some of the highest-paying and most competitive careers available to college graduates.

But many students struggle to understand the differences between major finance paths.

Some careers focus heavily on:

Others focus more on:

Understanding these differences early can help students make smarter long-term career decisions.

Investment banking remains one of the most prestigious finance careers.

Bankers work on:

The compensation can become extremely high, but the workload is also notoriously demanding.

Private equity professionals acquire companies and work to improve business performance.

The industry attracts many former investment bankers because of:

Hedge funds focus heavily on investing and market performance.

Professionals analyze:

Strong analytical ability is critical in this industry.

Venture capital focuses on startup investing and innovation.

Professionals work closely with founders and emerging companies.

The industry appeals strongly to people interested in:

Corporate finance roles exist inside major companies.

Professionals may work on:

These careers often provide more predictable lifestyles than Wall Street roles.

The best finance career depends heavily on:

Students should spend time learning how each industry actually operates before committing to a career path.

Applying to top MBA programs has become increasingly competitive.

Elite business schools receive applications from:

Strong applicants usually offer much more than impressive test scores.

Admissions teams look for:

Most elite MBA programs prefer candidates with meaningful professional experience.

Admissions teams want students who can contribute real-world insights inside the classroom.

Strong work experience often demonstrates:

Top MBA applicants usually explain:

Clear career direction makes applications significantly more compelling.

MBA admissions teams value leadership heavily.

Leadership can appear through:

Schools want students who can positively influence classmates and future organizations.

MBA essays often determine whether applicants feel memorable.

Strong essays usually sound:

Admissions officers read thousands of applications every year.

Generic essays rarely stand out.

Applicants should spend time researching:

Speaking with current students and alumni can provide valuable insight.

Successful MBA applications combine:

In highly competitive admissions environments, authenticity and preparation often matter more than applicants realize.

Few finance careers combine:

quite like mergers and acquisitions.

M&A banking sits at the center of some of the largest financial transactions in the world.

Professionals in this field advise companies on:

For MBA graduates and finance professionals, M&A remains one of the most prestigious and financially rewarding career paths on Wall Street.

But despite the compensation and prestige, the industry is also known for:

M&A bankers advise corporate executives and boards during major transactions.

Their responsibilities often include:

Bankers may work on:

The work combines both technical finance and high-level business strategy.

M&A recruiting is heavily concentrated among:

Bulge bracket firms typically offer:

Elite boutiques often focus more purely on advisory work and may provide:

Many finance professionals strongly prefer boutique M&A because of the intense advisory exposure.

Technical finance skills remain essential in mergers and acquisitions.

Professionals are expected to understand:

However, technical ability alone is rarely enough.

Top M&A professionals also develop:

The best bankers understand not only whether a deal works financially, but whether it makes strategic sense.

M&A compensation remains among the highest in finance.

Associates and vice presidents at top firms often receive:

However, compensation reflects the demanding nature of the work.

Long hours and unpredictable schedules remain extremely common.

M&A experience creates strong long-term career flexibility.

Professionals often transition into:

The transaction experience gained in M&A banking remains highly respected across finance.

Mergers and acquisitions continues to attract ambitious professionals because of its:

Students interested in M&A should focus heavily on:

Asset management remains one of the most intellectually demanding careers in finance.

Unlike investment banking, which focuses heavily on transactions, asset management revolves around:

Professionals in this industry manage money on behalf of:

For MBA graduates interested in investing rather than deal execution, asset management can become an incredibly rewarding long-term career path.

Asset managers analyze investment opportunities and allocate capital across:

Their primary objective is to generate strong long-term returns while managing risk.

Professionals may work in:

The industry rewards patience, discipline, and analytical thinking.

One of the biggest shifts in modern asset management is the growth of passive investing.

Passive investing focuses on:

Active management involves professionals attempting to outperform market benchmarks through:

Career experiences can differ significantly between these two models.

Strong investment professionals usually develop expertise in:

Communication skills also matter because investment ideas must often be defended clearly to:

Many successful professionals spend years refining their investment philosophy.

Compensation varies significantly depending on:

Portfolio managers at successful firms may eventually earn:

However, career progression in asset management is usually slower than many MBA graduates initially expect.

The path toward portfolio management often takes years.

Many professionals begin as:

Over time, they build:

Consistent analytical quality becomes far more important than short-term market luck.

Asset management remains one of the most respected long-term careers in finance.

Professionals who succeed in the industry often combine:

For MBA graduates interested in investing, the field can provide both intellectual satisfaction and substantial long-term upside.

If you spend enough time researching finance careers, eventually the same terms start appearing everywhere:

That’s not a coincidence.

For decades, top MBA programs have served as major recruiting pipelines into elite finance firms.

But here’s something many students discover too late:

not all MBA programs create the same career opportunities.

Some schools maintain deep recruiting relationships with:

Others offer strong academics but limited Wall Street access.

Understanding that difference can completely change a student’s career trajectory.

In industries like investment banking, recruiting remains heavily relationship-driven.

Top business schools provide:

Large banks continue recruiting aggressively from specific “target schools.”

That’s one reason elite MBA programs remain so influential in finance.

Wharton continues to dominate conversations around MBA finance recruiting.

The school maintains exceptionally strong relationships with:

Many professionals consider Wharton one of the strongest MBA brands in global finance.

Harvard Business School remains one of the most prestigious institutions in the world.

Its influence extends far beyond finance into:

Many students use Harvard to pivot into investment banking from:

Stanford offers extraordinary access to:

Its location creates strong opportunities for students interested in tech-focused finance careers.

MIT Sloan has become increasingly attractive for finance professionals interested in:

The combination of finance and technology continues becoming more valuable every year.

For students targeting international finance careers, both London Business School and INSEAD remain extremely powerful options.

These programs provide:

Compensation remains one of the biggest reasons professionals pursue investment banking careers.

MBA associates at top banks frequently earn:

However, the workload can become extremely demanding.

Many bankers continue working:

High compensation often comes with equally high pressure.

Top banks evaluate far more than intelligence alone.

Recruiters usually look for:

Technical interviews may include:

Behavioral interviews matter just as much.

Students interested in investment banking should become comfortable with:

Important concepts often include:

Strong technical preparation significantly improves recruiting performance.

Breaking into investment banking remains incredibly competitive.

But students who combine:

still create real opportunities for themselves.

The right MBA can dramatically accelerate that process.

And in 2026, elite business schools continue playing a major role in shaping the next generation of Wall Street professionals.

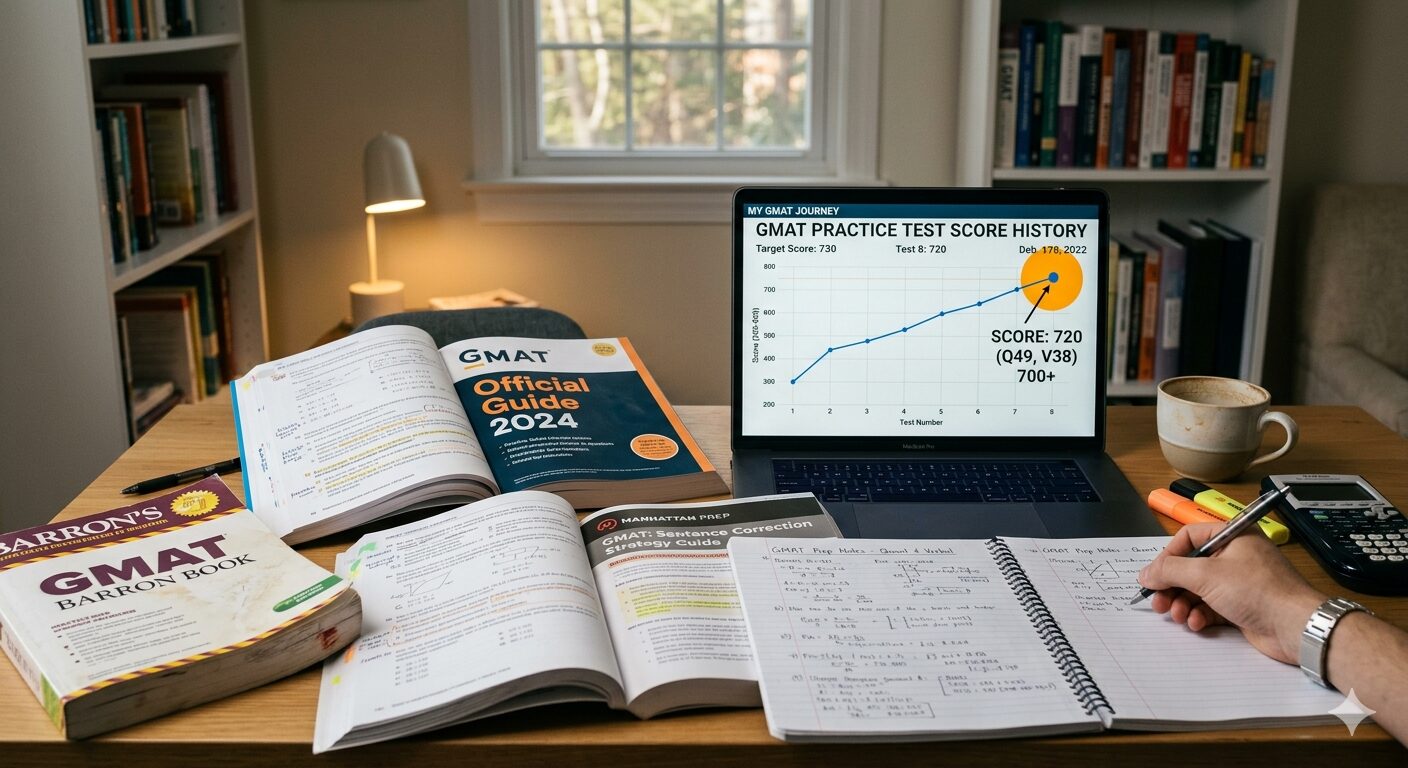

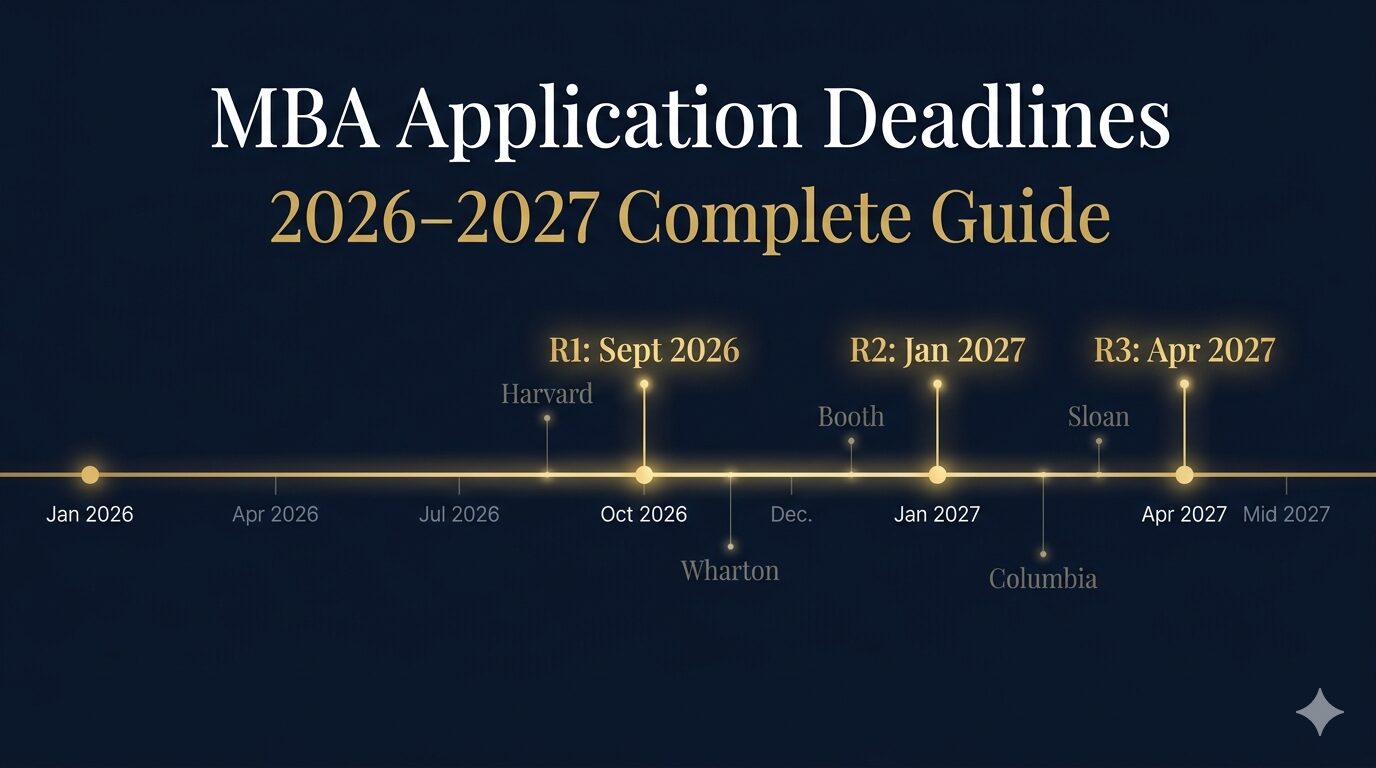

A 700+ GMAT score is the threshold that puts you in serious contention at every M7 program. The median at Wharton is 733. At Chicago Booth it is 730. At Harvard Business School it is 740. Getting above 700 does not guarantee admission — but scoring below it at a top finance program almost always requires an extraordinary compensating factor. The good news: 700 is achievable in 3 months for most working professionals, with the right structure and the right resources.

The GMAT rewards consistent, structured practice over cramming. Students who study 10 hours per week for 12 weeks consistently outperform students who study 30 hours per week for 3 weeks.

The GMAT Focus Edition (current since 2023) has three sections: Quantitative Reasoning, Verbal Reasoning, and Data Insights. Total score ranges from 205 to 805. Understanding what each section actually measures is the first step to studying efficiently — many candidates waste weeks on things the GMAT does not heavily weight.

Quantitative Reasoning tests problem-solving with algebra, arithmetic, and geometry at roughly a high-school level. The questions reward efficient reasoning, not computation speed. Students who try to brute-force every problem run out of time. Data Insights combines data sufficiency questions (a format unique to the GMAT) with multi-source reasoning and table analysis — it rewards logical thinking more than mathematical ability. Verbal Reasoning tests critical reasoning, reading comprehension, and sentence correction.

| School | Median GMAT (2025) | 80% Range | Finance Strength |

|---|---|---|---|

| Harvard Business School | 740 | 700–770 | Very strong |

| Wharton (UPenn) | 733 | 700–760 | Top finance MBA |

| Chicago Booth | 730 | 700–760 | Top quant/finance |

| MIT Sloan | 730 | 700–760 | Strong (fintech) |

| Columbia Business School | 729 | 700–760 | Top (NYC finance) |

| Stanford GSB | 738 | 700–770 | Strong (VC + PE) |

| Kellogg (Northwestern) | 727 | 690–760 | Strong |

| London Business School | 708 | 660–740 | Strong (Europe) |

| INSEAD | 703 | 650–740 | International |

Target a score at or above the median of your target schools. For M7 programs, 720+ is a strong score; 700–719 is competitive with other strong application elements. Every unnecessary retake slightly dilutes the result — admissions committees see your full score history. Plan to take the test once.

This plan assumes 8–12 hours of study per week — realistic for most working professionals. If you have more time, compress to 8 weeks. If less, extend to 16 weeks without changing the structure.

| Week | Focus | Key Activities | Hrs/Week |

|---|---|---|---|

| Week 1 | Diagnostic | Full official practice test. Identify weak sections. | 10 |

| Week 2–3 | Quant Foundations | Algebra, arithmetic, number properties. 50 OG problems/day. | 10 |

| Week 4–5 | Data Insights | Data sufficiency logic. Multi-source reasoning. Table analysis. | 10 |

| Week 6–7 | Verbal Foundations | CR argument structure. RC strategy. SC grammar rules. | 10 |

| Week 8–9 | Mixed Practice | Timed section drills. Error log review. Find persistent gaps. | 10 |

| Week 10–11 | Full Simulations | 2 full official practice tests. Review every wrong answer. | 12 |

| Week 12 | Final Prep | Light review, rest, logistics. Test day. | 6 |

The error log is non-negotiable. Every incorrect answer gets logged with: question type, why you got it wrong (concept gap, careless error, or time pressure), and the correct approach. Reviewing it weekly is how you stop repeating mistakes. Candidates who skip the error log plateau around 650 and cannot understand why their score does not improve.

The Quant section is where most candidates lose the most recoverable points. The content is high-school level; the difficulty is in time pressure and problem construction. The two most common failure patterns are: trying to calculate what should be estimated, and missing what a data sufficiency question is actually asking.

Data sufficiency questions always use the same five answer choices about whether Statement 1, Statement 2, or both are sufficient. This format is unique to the GMAT and requires a specific mental framework. Practice data sufficiency exclusively for at least 5 days before mixing it with other types — the reasoning pattern is different enough that mixing them early creates confusion.

Number properties — divisibility, primes, factors, and remainders — appear in 20–25% of Quant questions. One focused week on number properties typically yields a larger score improvement than any other single Quant topic. Start there if you are below 650 in Quant.

Critical Reasoning questions test argument analysis: identifying assumptions, strengthening or weakening conclusions, and spotting logical flaws. The most common mistake is choosing answers based on what sounds reasonable in the real world rather than what the argument strictly supports. The GMAT is a closed world — external knowledge is irrelevant and sometimes actively misleading. Evaluate only the evidence presented in the stimulus.

Reading Comprehension rewards active reading. Before answering questions, identify the main point of each paragraph and the passage's overall purpose in one sentence. RC errors almost always come from misremembering what the passage said versus what you assumed. The correct RC answer is always supported by specific language in the passage — if you cannot point to the supporting sentence, the answer is wrong regardless of how reasonable it seems.

Sentence Correction tests a finite set of grammar rules: subject-verb agreement, pronoun reference, parallel construction, modifier placement, and verb tense. Learning these 6 rule categories and recognizing them on sight eliminates 70–80% of SC errors. Answering SC by "ear" — choosing what sounds right — is unreliable. Identify the error, eliminate choices that do not fix it, and check for secondary errors among what remains.

Official GMAT materials from GMAC are the only resources that exactly replicate the real test. Always prioritize official materials for timed practice.

In the final week: stop new practice problems after day 3. Rest, review your error log one final time, and confirm test day logistics. Arriving tired costs more points than any last-minute studying can recover. The GMAT rewards a clear, rested mind more than a well-prepared exhausted one.

For decades, the MBA program at Harvard Business School has been considered one of the most prestigious business education experiences in the world. But many prospective students still ask the same question: what do students actually study inside the Harvard MBA program? The answer is far more interesting than most people expect. Unlike programs focused heavily on lectures and exams, HBS builds its MBA experience around real business decisions, leadership development, strategic thinking, and practical management training — and in 2026, the curriculum is evolving faster than at any point in its history.

Harvard does not just teach business — it trains executives to make high-stakes decisions under uncertainty. That distinction is why the HBS network remains the most powerful in the world 75 years after the program was founded.

The Harvard MBA is a two-year, full-time, general management program divided into two distinct phases. The first year is a required, shared curriculum — every student in the class takes the same core courses together. The second year is almost entirely elective, allowing students to specialize deeply in finance, entrepreneurship, technology, or any other domain. This structure is intentional: Harvard believes that effective general managers need breadth before they earn the right to specialize. A first-year finance student sits next to a former military officer, a doctor, and a startup founder — and the diversity of perspectives in case discussions is itself part of the curriculum.

Students move through the first year in assigned groups called sections of approximately 90 students. The section becomes your primary community for the first year — you take every class together, study together, and develop the kind of intense professional relationships that define the HBS alumni network for decades afterward. The section model also means that participation and communication skills are developed under real social pressure, not in anonymous online forums.

The first-year required curriculum covers the full breadth of general management. For finance-focused students, the Finance I and Finance II courses are the most directly relevant, but the curriculum is designed so that every course contributes to a student's ability to evaluate and lead complex organizations.

| Course | Core Focus | Finance Relevance |

|---|---|---|

| Finance I & II | Corporate finance, valuation, capital allocation | Very High — direct IB/PE preparation |

| Financial Reporting & Control | Accounting, financial statements, GAAP | Very High — essential for all finance roles |

| Strategy | Competitive dynamics, market positioning | High — M&A and corporate strategy |

| Leadership & Org. Behavior | Team dynamics, executive decision-making | Medium — client and team management |

| Technology & Operations | Digital transformation, supply chains | Medium — fintech and operational finance |

| Marketing | Customer behavior, pricing, branding | Low-Medium — useful for corporate roles |

| Data Science & AI for Leaders | Machine learning, business analytics | High — quant finance and fintech |

| FIELD Immersion | Real-world project with global company | Medium — client interaction skills |

Finance I and Finance II together form the analytical backbone of the HBS experience for students targeting investment banking, private equity, or hedge funds. The courses cover corporate finance fundamentals, discounted cash flow valuation, capital structure decisions, and investment analysis. What distinguishes these courses from standard finance education is the case method delivery — students do not just learn to apply the DCF formula, they debate whether a specific CEO made the right capital allocation decision in a real transaction, with classmates who may have been the banker or consultant on the deal.

One of the most significant curriculum shifts in recent years is the expansion of AI and data science education. The course Data Science and AI for Leaders, now a required first-year component, helps students understand machine learning applications, business analytics, AI-driven decision-making, and the strategic impact of artificial intelligence across industries. This is not a programming course — HBS does not train software engineers. It trains executives to ask the right questions of technical teams, evaluate AI-driven business models, and understand where machine learning creates genuine competitive advantage versus where it is organizational noise.

For finance students specifically, this matters enormously. Quantitative hedge funds, systematic trading firms, and the data science teams at major banks are hiring MBA graduates who can bridge the gap between finance domain expertise and algorithmic thinking. An HBS graduate who combines Finance I/II knowledge with a genuine understanding of machine learning applications is more valuable to these employers in 2026 than a pure quant or a pure finance MBA graduate.

The Harvard case method is one of the most discussed and least understood features of the HBS experience. Rather than traditional lectures, students analyze real business situations and discuss executive decisions, strategic mistakes, leadership challenges, and financial outcomes. During the MBA, students analyze approximately 400 to 500 business cases — real companies, real decisions, real consequences. Each case is typically 15-25 pages of primary source material: financial statements, board memos, market data, and management interviews.

Class participation is not optional — it is graded and typically represents 50% of the course grade. The professor cold-calls students to open a case discussion, and that student must analyze the situation and make a clear recommendation in front of 90 peers. This creates an environment where communication, intellectual confidence, and the ability to synthesize complex information quickly become survival skills rather than optional soft skills. For students targeting client-facing finance careers — investment banking, PE, consulting — this is arguably the most valuable preparation the MBA provides that cannot be replicated through technical training alone.

During the second year, students choose from more than 100 elective courses and independent projects. The flexibility is significant — a student focused on private equity can spend their entire second year on PE-specific courses, deal analysis projects, and independent research with a faculty member. Popular finance-related electives include courses in leveraged buyouts, venture capital and private equity, real estate investment, securities analysis, and financial crises. The Entrepreneurial Finance course is consistently one of the most popular in the school, reflecting the overlap between HBS's finance strength and its entrepreneurial culture.

Harvard also offers joint degree programs combining the MBA with law (JD/MBA), public policy (MPP/MBA), and engineering (MS/MBA). The MS/MBA program run jointly with the Harvard John A. Paulson School of Engineering is particularly relevant for students targeting fintech, quantitative finance, or technology-focused investment roles where deep technical credentials complement the business training.

The Harvard MBA remains one of the most powerful business credentials in the world — but its value is not uniform across career paths. For students targeting investment banking, consulting, or entrepreneurship, the HBS brand and alumni network provide advantages that are difficult to quantify but consistently visible in recruiting outcomes. Major investment banks, strategy consulting firms, and venture capital funds actively recruit at HBS and treat HBS graduates as a pre-screened, high-quality talent pool. That institutional relationship — built over decades — is not easily replicated by any other program.

The honest caveat: at $76,000 per year in tuition plus living expenses, the Harvard MBA costs over $230,000 in direct expenses, plus two years of foregone income. The NPV calculation is positive for most HBS graduates — median post-MBA compensation exceeds $175,000 in base salary alone — but it requires a career trajectory that actually captures the premium the degree commands. Students who use Harvard to pivot into high-compensation finance roles recover the investment within 3-5 years. Students who use it to enter non-profit or government roles may find the ROI considerably more modest.

When people talk about the best MBA programs for finance careers, one name appears almost every time: Wharton. The Wharton School at the University of Pennsylvania has built one of the strongest reputations in the world for finance education, analytical business training, leadership development, and Wall Street recruiting. But many prospective students still wonder — what do Wharton MBA students actually study? The answer goes far beyond spreadsheets and corporate finance. The Wharton MBA curriculum is designed to combine analytical rigor, leadership development, communication skills, and deep career specialization — and in 2026, the program continues evolving around artificial intelligence, business analytics, global markets, and technology-driven finance.

Wharton does not just teach finance — it trains professionals to apply analytical frameworks to every business problem they encounter. That combination of depth and breadth is why Wharton graduates consistently appear at the top of Wall Street, consulting, and PE recruiting pipelines.

The Wharton MBA is a two-year, full-time, highly customizable graduate business program. Students must complete 19 course units (CUs) during the MBA. Unlike Harvard's section-based, case-method model, Wharton gives students significantly more flexibility in structuring their curriculum from the beginning. The program is divided into three major sections: the Core Curriculum, Majors and Specializations, and Elective Courses. This structure allows students to build strong business fundamentals while customizing the MBA tightly around specific career goals — which is one reason Wharton consistently attracts a high concentration of finance-focused students who want both analytical depth and recruiting access.

The first major component is the Wharton Core Curriculum, which builds foundational knowledge across leadership, economics, finance, marketing, communication, and analytics. The core is divided into the Fixed Core (first semester) and the Flexible Core (where students choose within defined disciplines).

| Course | Type | Core Focus | Finance Relevance |

|---|---|---|---|

| Foundations of Teamwork & Leadership | Fixed | Collaboration, executive communication | Medium — client and team management |

| Marketing Management | Fixed | Customer behavior, pricing, branding | Low-Medium |

| Microeconomics for Managers | Fixed | Pricing dynamics, competitive markets | High — macro/micro for finance |

| Regression Analysis for Managers | Fixed | Statistics, data-driven decisions | High — quant finance foundation |

| Management Communication | Fixed | Presentations, business writing | High — IB and PE client work |

| Corporate Finance | Flexible | Valuation, capital structure, M&A | Very High — IB/PE core skill |

| Accounting | Flexible | Financial statements, GAAP | Very High — essential for all finance |

| Macroeconomics | Flexible | Interest rates, global markets | High — markets and macro investing |

| Business Analytics | Flexible | AI, machine learning, data strategy | High — quant and fintech roles |

The Regression Analysis for Managers course deserves specific mention for finance students. Unlike programs where statistics is treated as an optional or supplementary skill, Wharton makes quantitative data analysis a fixed core requirement. This reflects Wharton's broader philosophy that rigorous analytical thinking — not just financial modeling — is the foundation of effective business leadership. Students who enter Wharton with stronger quantitative backgrounds can opt into advanced versions of core courses, allowing them to move faster toward specialized finance electives.

One of Wharton's biggest competitive advantages is the depth of its specialization system. Students must complete at least one MBA Major, chosen from approximately 18 to 20 concentration areas. The Finance Major is by far the most popular, attracting a large share of the class each year. Within the Finance Major, students take a series of courses covering corporate finance, investment management, financial derivatives, real estate finance, and advanced valuation. The breadth within the single major is comparable to what other schools offer across their entire elective catalog.

Other popular majors with strong finance overlap include Business Analytics (increasingly valuable for quant roles and fintech), Real Estate (for students targeting real estate PE and REITs), and Entrepreneurship & Innovation (for VC-focused students). Students can also combine majors — a Finance + Business Analytics double major is increasingly common among students targeting quantitative hedge funds, systematic trading firms, or fintech leadership roles where analytical credibility is as important as finance domain knowledge.

Wharton's recruiting outcomes in finance are consistently at the top of the M7. Goldman Sachs, JPMorgan, Morgan Stanley, Evercore, Lazard, and virtually every major PE and hedge fund actively recruit at Wharton and treat it as a primary target school. The reasons are structural: Wharton has the largest Finance alumni network in elite finance, a finance faculty that includes active practitioners and Nobel laureates, and a student culture where finance career preparation is deeply embedded in the first-year experience.

The Wharton Finance Club is one of the most active professional organizations in any MBA program — it runs technical training workshops, PE recruiting prep sessions, and direct alumni networking events that begin in the first weeks of the first year. Students who arrive at Wharton planning to enter investment banking or PE typically start building their recruiting relationships before the first semester is over, which is the correct timeline given that formal recruiting begins in January of the first year.

Wharton offers more than 200 elective courses, allowing students to build highly specific academic pathways. Students may also take courses across other University of Pennsylvania graduate schools — the Law School, the Engineering School, and the School of Arts and Sciences — creating genuinely interdisciplinary options that no other M7 program can match at scale. Global learning is integrated throughout the MBA through international business projects, global immersions, and cross-border case studies. As finance and consulting become increasingly global, the ability to navigate cross-cultural business environments is a genuine differentiator in senior leadership roles.

Summer internships between the first and second year are treated as the primary recruiting pipeline by most employers. Students who secure internships at Goldman Sachs, Blackstone, or McKinsey in the summer after first year receive full-time offers at the end of the internship in the vast majority of cases — making that summer the most career-critical period of the MBA. Wharton's placement rate in competitive summer internships consistently ranks among the highest in the country, a reflection of both the school's recruiting relationships and the preparation quality of its students.

For students targeting finance careers, Wharton is arguably the single most powerful MBA credential available. The combination of the Finance Major, the Wall Street recruiting network, the Wharton alumni base in PE and hedge funds, and the quantitative analytical training creates an educational product that is genuinely differentiated from even other M7 programs. Tuition runs approximately $84,000 per year, making the two-year cost over $240,000 before living expenses — but post-MBA compensation for finance-track Wharton graduates consistently exceeds $300,000 in the first year, making the investment financially justifiable for most students on that career path.

The honest caveat is admission: Wharton's acceptance rate is below 15%, and the median GMAT is 733. Successful applicants typically combine 3-7 years of strong professional experience, demonstrated leadership, and a clear career narrative that explains why Wharton specifically — not just "an elite MBA" — is the right next step. Candidates who can articulate the specific Wharton resources, courses, and alumni relationships they plan to leverage are consistently more competitive than equally credentialed candidates who treat Wharton as one application among many.

Find out if an MBA is worth it — and exactly when you will break even on your investment.

Fill in your details and click Calculate My ROI to see your personalized breakdown.

From LBO to WACC — every term you need to know for MBA interviews, finance careers and Wall Street.

Compare two top MBA programs side by side — cost, salary, finance placement and more.

Select two schools above to start comparing

Cost, salary, GMAT scores, finance placement and more — all side by side.

Test your knowledge across 30 questions — 15 Investment Banking technical and 15 GMAT quantitative.

Select a category or take the full 30-question challenge.

20 proven steps to break into investment banking — used by candidates at Harvard, Wharton and Columbia.

Enter your email and download the checklist immediately — no spam, ever.

Trusted by finance candidates at

Harvard • Wharton • Columbia • Booth • NYU Stern

The rise of AI has triggered a genuine crisis of confidence among prospective MBA students. If ChatGPT can write a memo, build a financial model, and summarize an earnings call in seconds, what exactly are $200,000 and two years of your life buying you? It is a legitimate question — and one that deserves a direct, data-grounded answer rather than reassuring platitudes from business school admissions offices. The honest 2026 answer is nuanced: AI is meaningfully changing what finance professionals do, but the career credentials, network access, and leadership development that a top MBA provides have become more valuable, not less, in an AI-accelerated world.

AI is reshaping finance workflows — but the humans directing those workflows still need judgment, relationships, and institutional credibility. That is exactly what a top MBA is designed to build.

In 2026, every prospective MBA student is confronting the same uncomfortable question: does a $200,000+ degree still make sense when AI tools can perform many of the analytical tasks that used to require years of expensive education? The anxiety is real, but it is also somewhat misdirected. AI is automating tasks — specific, repeatable, data-processing tasks. It is not automating careers, judgment, relationships, or organizational credibility. Understanding the difference is critical to making a rational decision about graduate business education.

The MBA's value proposition has always rested on three pillars: skills, network, and credential. AI is affecting the first pillar at the margins — certain technical tasks are becoming easier. But the credential and network pillars are completely unaffected by AI adoption, and if anything, they are becoming more valuable as the supply of AI-proficient workers grows and employers increasingly differentiate based on leadership capacity and institutional trust rather than technical execution alone.

The right question is not whether AI replaces the MBA. The right question is whether an MBA still provides a sufficient return on a $200k+ investment for your specific career goals. For investment banking, private equity, consulting, and corporate leadership tracks, the answer in 2026 remains yes — with important caveats about program selection and career fit.

AI is genuinely automating a meaningful portion of the work that junior finance professionals once performed manually. Document review, data extraction from financial statements, first-draft financial model construction, earnings call transcription and summarization, covenant compliance checking in credit agreements — these tasks are being partially or fully automated across investment banks, PE firms, and asset managers. Junior analysts at bulge-bracket banks are reporting that AI tools now handle work that previously consumed 30-40% of their working hours.

This is real and consequential. But it is important to recognize what this automation actually means for MBA value: it means that the lower-level analytical grunt work that used to justify hiring large analyst classes is shrinking. Firms need fewer people doing data entry and first-pass modeling. They need more people who can interpret, contextualize, advise, and lead — which is precisely the skill set that MBA programs are designed to develop. The automation of junior-level tasks does not make the MBA irrelevant; it makes the judgment and leadership development that MBAs provide more valuable at the margin.

There are entire categories of high-value finance work that AI cannot perform in 2026 and is unlikely to perform well for many years. Client relationship management requires trust, emotional intelligence, and institutional credibility that no language model can credibly replicate. Deal negotiation involves real-time reading of human psychology, power dynamics, and organizational politics. Investment thesis development at the highest level requires the synthesis of qualitative judgment with quantitative analysis in ways that remain fundamentally human. Managing teams through uncertainty, communicating complex ideas to boards, structuring novel deal terms — these are all deeply human activities.

Leadership, in particular, is an area where AI has essentially no footprint. PE portfolio company CEOs, investment committee chairs, and managing directors at major banks are not being replaced by AI — they are using AI to make their existing teams more productive. The people in those senior roles came through MBA programs, not because the MBA taught them Python, but because it taught them how to operate credibly in high-stakes institutional environments. That skill is completely orthogonal to what AI does.

The MBA alumni network argument has always been made by business schools, and it has always been somewhat overstated in marketing materials. But in 2026, the network component of a top MBA is genuinely undervalued by prospective students. As AI compresses the technical skill differentials between candidates — if everyone can build a DCF in minutes using AI tools, the technical moat shrinks — what differentiates candidates increasingly comes down to relationships, referrals, and institutional trust.

Harvard, Wharton, and Booth graduates are not getting hired at Goldman Sachs and Blackstone because they learned financial modeling in business school. They are getting hired because alumni already inside those firms vouch for them, because recruiters have 30-year relationships with those schools, and because the credential signals a specific level of institutional selectivity that firms use as a proxy for candidate quality. AI does nothing to undermine this dynamic — if anything, it intensifies it, because the credential becomes a more important signal when technical skills are increasingly commoditized.

The practical implication is that the MBA network compounds over a career in ways that are difficult to quantify at the time of enrollment but become unmistakably clear by year ten. Board seats, LP relationships, senior hiring decisions, and strategic partnership introductions disproportionately flow through MBA alumni networks. That advantage is completely unaffected by the rise of AI language models.

| Program | Total Cost | Avg Post-MBA Salary | Break-Even |

|---|---|---|---|

| Harvard HBS | $230,000 | $175,000 | 3–4 years |

| Wharton | $225,000 | $172,000 | 3–4 years |

| Chicago Booth | $215,000 | $165,000 | 3–4 years |

| Kellogg | $210,000 | $158,000 | 4–5 years |

| Yale SOM | $200,000 | $150,000 | 4–5 years |

These numbers tell a clear story for candidates targeting finance, consulting, and leadership tracks: the break-even is 3-5 years, and the 10-year net present value of the investment is substantially positive for most M7 graduates who pursue the right career paths. The salary premium from a top MBA over a non-MBA career trajectory at the same starting point typically runs $50,000-$100,000 per year in finance — a premium that compounds significantly over a 20-year career. For a full program-by-program comparison, see our guide on Harvard MBA vs. Wharton MBA for Finance careers. The ROI math has not fundamentally changed in 2026.

An MBA is clearly worth it in 2026 for several specific profiles. Career switchers moving into investment banking, private equity, or management consulting from unrelated fields almost always need an MBA from a target school — there is no other credible pathway into these careers at the post-analyst level without the institutional credential. Candidates targeting senior leadership roles in corporate finance, strategy, or general management benefit enormously from the MBA's combination of credential signaling and network development. International candidates looking to break into the US finance market use M7 MBAs as the primary mechanism for obtaining recruiting access that would otherwise be completely unavailable to them.

The strongest 2026 candidates are those who combine MBA credentials with genuine AI competency — not the ability to use ChatGPT, but the ability to integrate AI tools into financial workflows, evaluate AI-generated analysis critically, and build processes that leverage AI while retaining human judgment at decision points. Programs like Wharton, Booth, and MIT Sloan are actively incorporating AI education into their curricula, which increases the value of attending specifically those programs for candidates who want both credentials.

The MBA is not worth it for everyone. Candidates who already have strong recruiting access to their target role — software engineers at top tech companies, for example, or finance professionals already in PE or hedge funds — often find that the opportunity cost of two years out of the workforce, plus $200k in tuition and foregone income, does not justify the credential. The MBA is a tool for gaining access and making career transitions; if you do not need either, the financial case weakens considerably.

Candidates targeting roles where the MBA credential is not a meaningful differentiator should also think carefully. Technical roles in quantitative finance, systematic trading, and data science increasingly value advanced degrees in mathematics, statistics, or computer science over business education. And entrepreneurs who are already building companies rarely benefit from the two-year interruption that a full-time MBA requires, particularly when alternative credentials and accelerator networks are available without the full program cost.

The honest 2026 verdict is this: a top MBA remains one of the highest-ROI educational investments available for candidates targeting finance, consulting, and leadership careers — but only from programs with genuine recruiting power and alumni network depth. AI has not changed this calculation in any fundamental way. What it has changed is the adjacent skill set that the strongest candidates bring alongside their MBA credential. The MBA graduate who also understands how to deploy AI tools in financial workflows, evaluate AI-generated analysis, and lead AI-augmented teams is meaningfully more valuable than the MBA graduate who treats AI as a threat rather than a tool.

The MBA application cycle for 2027 entry will be competitive regardless of what AI does to individual tasks. If you are targeting Goldman Sachs, Blackstone, McKinsey, or a top corporate leadership role, the credential from a top-8 program is still the most reliable path to that outcome. The question is not whether to get an MBA in the age of AI — it is whether your target program has the recruiting relationships, alumni network, and curriculum quality to justify the investment. For Harvard, Wharton, Booth, Kellogg, and their M7 peers, the answer remains yes.

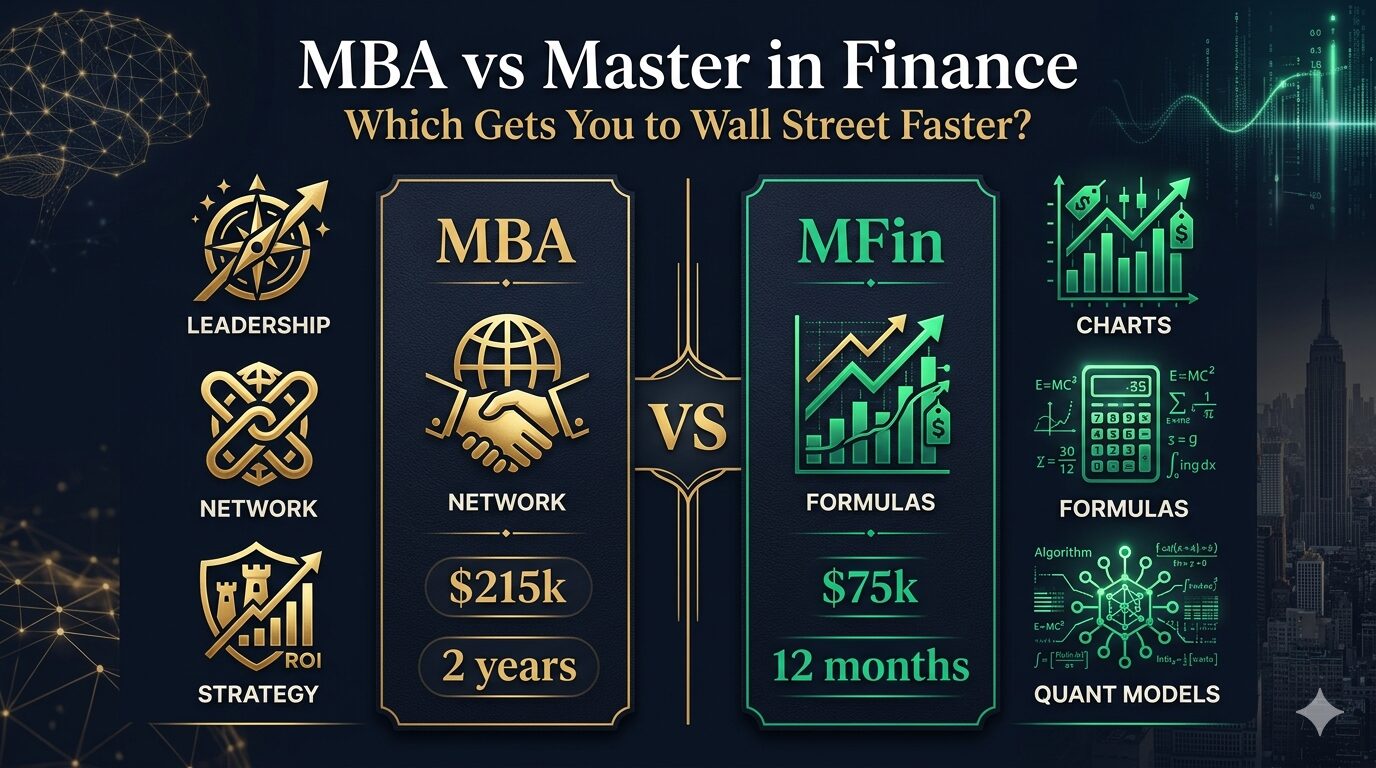

Two graduate degrees dominate the conversation for candidates targeting Wall Street: the MBA and the Master in Finance. They serve overlapping but distinct audiences, and choosing the wrong one for your profile and career goals can cost you years of time and six figures in avoidable tuition. The decision is more nuanced in 2026 than it has ever been — because the MBA is evolving to compete more directly with specialized finance degrees, while top MFin programs are expanding their recruiting relationships to reach employers that once recruited exclusively from MBA programs.

The MBA and the MFin are not interchangeable. One is designed for career changers and future leaders. The other is designed for technically minded recent graduates who want deep finance specialization fast. Your choice should start with honest self-assessment about where you are, not where you want to end up.

Both the MBA and the Master in Finance can lead to careers at investment banks, PE firms, asset managers, and hedge funds. But they get there via completely different mechanisms, serve different candidate profiles, and create different types of institutional capital. The MBA is a generalist leadership credential that happens to open specific finance doors through its recruiting network. The MFin is a specialized technical degree that provides deep quantitative finance training and increasingly strong placement at specific finance employers — particularly in technical and quantitative roles.

The most common mistake candidates make is treating this as a prestige comparison — asking which degree is "better" — rather than a fit question: which degree is right for my specific experience level, financial situation, and target career path? A recent college graduate targeting a quant trading role at Jane Street is almost certainly better served by a Princeton MFin than a Harvard MBA. A career-changer with five years in consulting who wants to move into PE is almost certainly better served by a Wharton MBA. The degree that matches your situation produces a dramatically better return than the nominally more prestigious degree that does not.

The Master in Finance is a specialized graduate degree focused on advanced financial theory, quantitative methods, and technical finance skills. Top programs include Princeton's Bendheim Center MFin, MIT Sloan's Master of Finance, London Business School's Master in Finance, and HEC Paris's Master in Finance. These programs typically run 10-16 months and admit students with limited professional experience — often directly from undergraduate programs or with one to three years of work experience. The curriculum is heavily quantitative: derivatives pricing, fixed income analysis, portfolio theory, financial econometrics, and risk management are core components.

The MFin is not a watered-down MBA. At programs like Princeton and MIT, it is a rigorous, mathematically demanding degree that prepares students for roles that require genuine quantitative depth. Graduates enter investment banking sales and trading, quantitative research, risk management, and increasingly asset management roles where analytical sophistication is the primary differentiator. The credential is well understood by sophisticated financial employers and is treated with significant respect in quantitative and trading-oriented hiring contexts.

The MBA is a two-year general management degree with broad applicability across industries and functions. Unlike the MFin, it is explicitly designed for candidates with meaningful professional experience — typically 3-7 years — who want to either change careers or dramatically accelerate their trajectory in their existing field. The MBA curriculum covers finance, marketing, operations, leadership, strategy, and organizational behavior. At M7 programs, the finance elective catalog is genuinely deep, but the foundation is breadth and leadership development rather than technical finance specialization.

The MBA's primary mechanism for creating career outcomes is its recruiting ecosystem, not its curriculum. The on-campus recruiting relationships that Harvard, Wharton, Booth, and Kellogg maintain with Goldman Sachs, McKinsey, Blackstone, and their peers are the core product being purchased. A Wharton MBA graduate entering investment banking is not competing on technical superiority over MFin graduates — they are entering through a recruiting channel that is specifically reserved for MBA students from target programs, with different interview formats, offer timelines, and expectations.

| Factor | MBA | Master in Finance |

|---|---|---|

| Duration | 2 years | 10–12 months |

| Total Cost | $200k–$230k | $60k–$90k |

| Work Exp Required | 3–7 years | 0–3 years |

| Curriculum Focus | Broad / Leadership | Technical / Quant |

| Network Size | Very large | Smaller, specialized |

| IB Recruiting Access | Strong at M7 | Moderate |

| PE / VC Access | Strong | Limited |

| Best For | Career switchers | Recent graduates |

| ROI Timeline | 3–5 years | 1–2 years |